Premium Financing Life Insurance A Strategy for Estate Liquidity Planning

Understanding Estate Liquidity Challenges

Many successful families accumulate wealth through businesses, real estate portfolios, and long term investment strategies. While these assets may represent significant net worth, they often provide limited immediate liquidity.

Federal estate taxes may reach up to 40% of an estate, and payment is generally due within nine months after death. When a large portion of wealth is concentrated in illiquid assets, heirs may face difficult decisions when estate taxes become due.

In certain situations, families may be forced to sell businesses, real estate, or investment assets in order to raise the funds necessary to satisfy estate tax obligations.

Estate liquidity planning seeks to address this challenge by evaluating strategies designed to ensure that sufficient liquidity may be available when future obligations arise.

One strategy that is sometimes considered within sophisticated estate planning discussions is premium financing life insurance.

Working alongside Estate Attorneys, CPAs, and Wealth Advisors.

-

Designed for $5M+ Net Worth

-

Earn $300K+ Annual Income

-

Maintain Long Term Planning Horizons

-

Hold Wealth in Illiquid Assets such as Businesses or Real Estate

Premium financing strategies require careful evaluation and are not appropriate for every financial situation. These structures are typically considered within broader estate liquidity planning discussions and should be evaluated alongside a client’s estate planning attorney, tax advisor, and financial professionals. The objective of this review process is to determine whether the strategy aligns with the client’s long term financial goals, balance sheet strength, and estate planning framework.

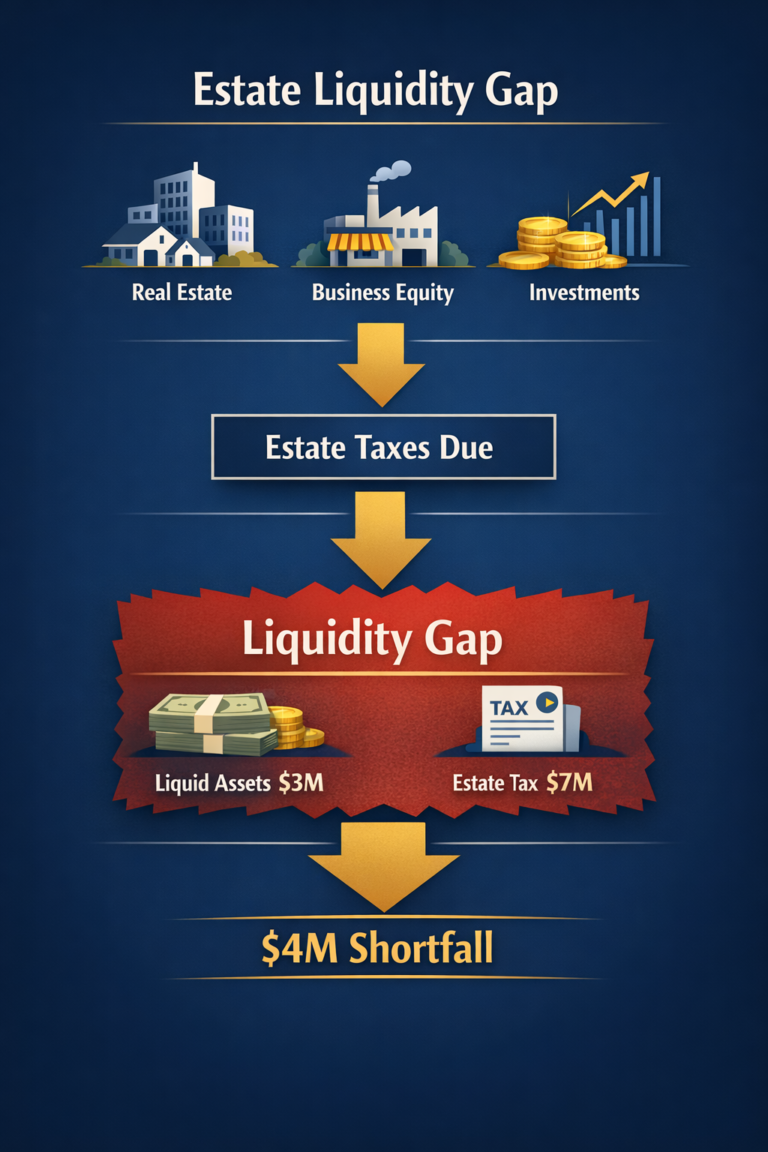

The Estate Liquidity Problem

When Net Worth Does Not Equal Liquidity

High net worth individuals frequently build wealth through assets such as:

-

Privately Held Businesses

-

Real Estate Investments

-

Private Equity Participation

-

Concentrated Stock Positions

Although these assets may generate substantial long term value, they may not be easily converted into cash without disrupting the underlying investment strategy.

When estate taxes become due, families without adequate liquidity may face the possibility of forced asset sales during unfavorable market conditions.

Estate Liquidity Problem Diagram

This diagram illustrates how an estate liquidity gap may occur when a family’s total net worth is largely tied to illiquid investments while estate tax obligations require immediate cash. Estate liquidity planning evaluates strategies that may help bridge this gap.

What Is Premium Financing?

Premium financing is a strategy in which a third party lender provides financing for life insurance premiums rather than the policy owner paying those premiums directly from personal assets.

The strategy is often evaluated within the context of estate liquidity planning when individuals wish to preserve investment capital while establishing life insurance coverage designed to provide future liquidity.

In many structures, a lender finances the insurance premiums while the policy is owned by a trust that is structured within the estate plan.

The goal is to allow the policy to generate liquidity that may ultimately help address estate tax obligations.

Premium Financing Structure Flow Diagram

This diagram illustrates the structural flow of a premium financing strategy. A lender provides financing for life insurance premiums while the policy is structured to generate liquidity for the trust that owns the policy. The trust may then use those proceeds to help satisfy estate tax obligations.

Why Estate Liquidity Planning Matters

Estate tax obligations may arise quickly after death, creating pressure for families whose wealth is concentrated in long term investments.

Without proper planning, heirs may face the challenge of selling businesses or real estate assets simply to meet tax obligations.

Estate liquidity strategies seek to reduce the likelihood that valuable family assets must be liquidated under time pressure.

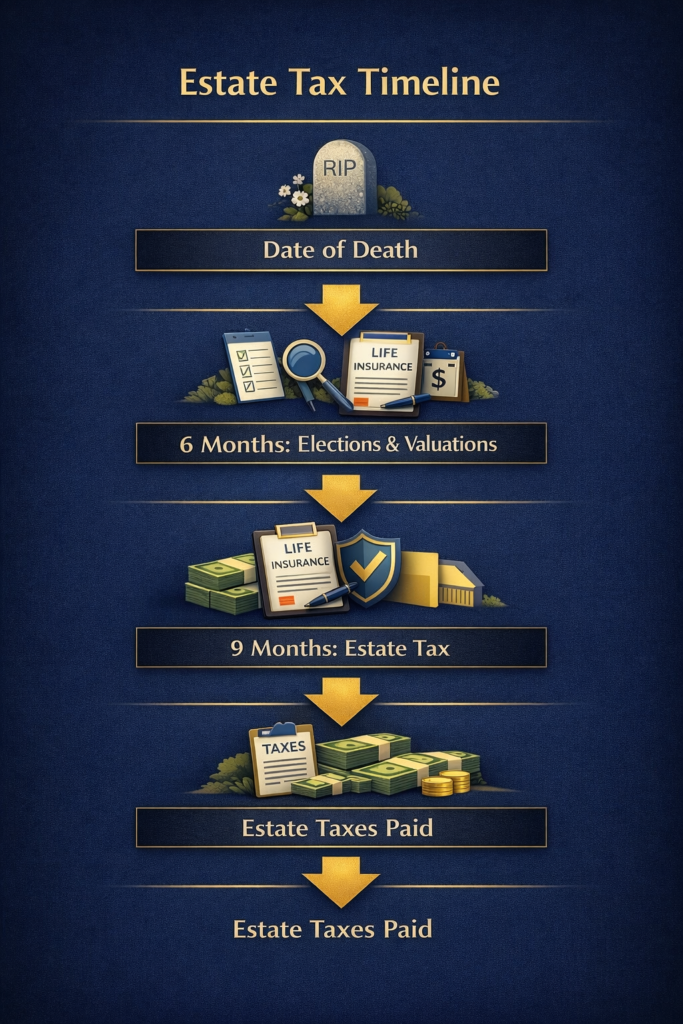

Estate Tax Timeline Diagram

This diagram illustrates the timeline associated with federal estate tax obligations. Because taxes may be due within nine months after death, planning for estate liquidity well in advance is often an important consideration for families with substantial illiquid assets.

When Premium Financing May Be Considered

Premium financing strategies are most commonly evaluated for individuals and families whose wealth is concentrated in long term investments or illiquid assets and who are engaged in proactive estate planning.

These may include individuals who:

-

Have Significant Net Worth Relative to Liquid Assets

-

Maintain Substantial Real Estate or Business Holdings

-

Expect Potential Estate Tax Exposure

-

Prefer to Preserve Investment Capital Rather than Redirect Assets to Insurance Premiums

-

Have Long Term Planning Horizons

Each situation must be evaluated individually to determine whether financing structures may be appropriate.

Situations Where Alternative Strategies May Be More Appropriate

Premium financing may not be appropriate in all circumstances. In certain situations, alternative estate planning strategies may be more suitable depending on a client’s financial profile, liquidity position, or planning objectives.

Examples may include situations where:

-

Liquidity is Already Sufficient to Address Estate Obligations

-

Balance Sheet Strength Does Not Support Financing Structures

-

Investment Volatility Could Affect Collateral Stability

-

Long Term Financing Structures May Not Align with Planning Preferences

Evaluating these factors helps ensure that premium financing strategies are considered within a broader financial planning framework.

Importance of Advisor Coordination

Estate liquidity planning strategies often involve coordination among multiple professionals, including estate planning attorneys, certified public accountants, insurance carriers, and lending institutions.

Strategic Premium Finance works alongside these professionals to help evaluate whether premium financing structures align with the client’s estate planning objectives while ensuring the strategy is considered within a comprehensive advisory framework.

Our Estate Liquidity Planning Process

A Structured Approach to Strategy Evaluation

Strategic Premium Finance follows a structured evaluation process designed to help families and their advisors explore whether premium financing strategies may fit within broader estate planning objectives.

- No pressure.

- No product pushing.

- Only clarity and alignment.

Estate liquidity planning is most effective when evaluated well before potential tax obligations arise. Strategic Premium Finance works alongside clients and their advisors to explore whether structured premium financing strategies may fit within a comprehensive estate planning framework.

Strategic liquidity planning helps prevent these forced decisions.

Many successful families accumulate wealth through businesses, real estate portfolios, or long term investment strategies. While these assets may represent significant net worth, they often provide limited liquidity when large financial obligations arise.

Estate taxes, business succession planning, and generational wealth transfer can all require significant liquidity at specific moments in time. Without careful planning, families may face the difficult decision of selling valuable assets to meet those obligations.

Potential Exit Strategies

Premium financing strategies typically include planning for eventual repayment of the financing.

Possible exit strategies may include:

policy cash value accumulation

refinancing structures

policy maturity

death benefit proceeds

Premium Financing Exit Strategy Diagram

This diagram explains potential exit strategies for premium financing structures including loan repayment through policy cash value, policy maturity, or death benefit proceeds.

Important Considerations and Risk Factors

Premium financing introduces financial leverage and therefore requires careful evaluation.

Premium financing introduces financial leverage and therefore requires careful evaluation. While the strategy may offer planning benefits in certain circumstances, it also involves risks that should be carefully considered as part of a broader estate planning discussion.

Factors that must be considered include:

Because of these considerations, premium financing strategies are typically evaluated only within comprehensive estate planning discussions involving qualified advisors.

When Premium Financing May Be Considered

Premium financing strategies are typically evaluated in situations where clients:

Have substantial net worth

Maintain strong income or balance sheet strength

Wish to preserve investment capital

Face potential estate tax exposure

Are engaged in long term estate planning

These structures are not appropriate for every situation and require careful analysis before implementation.

How the Strategy Is Structured

Premium financing arrangements typically involve several coordinated components:

Strategic Premium Finance follows a disciplined evaluation framework known as the Estate Liquidity Blueprint.

- No pressure.

- No product pushing.

- Only clarity and alignment.

Estate Tax Timeline Diagram

This diagram shows the estate tax timeline highlighting the nine month deadline for federal estate tax payments and the importance of liquidity planning before estate settlement.

Request a Confidential Strategy Session

If you’re exploring whether premium financing could fit into your broader planning strategy, the first step is a brief confidential consultation.

No obligation. Just clarity.

Book Your Free Private Strategy Call

Confidential. No obligation.

- (305) 903-0363

- Marc@strategicpremiumfinance.com

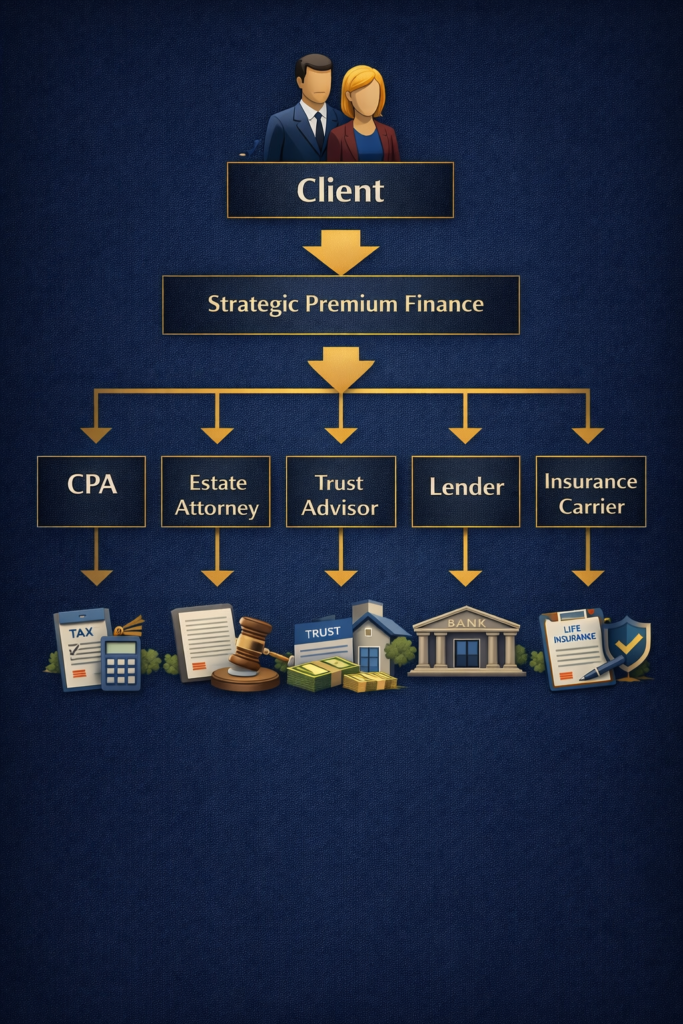

Coordination With Professional Advisors

Premium financing strategies require collaboration among multiple professionals, including:

-

Estate Planning Attorneys

-

Certified Public Accountants

-

Insurance Carriers

-

Lending Institutions

-

Trust Advisors

Strategic Premium Finance works alongside a client’s existing advisory team to evaluate whether premium financing structures may align with the client’s long term planning objectives.

Advisor Coordination Diagram

This diagram illustrates the collaborative structure of estate liquidity planning involving financial advisors, estate attorneys, CPAs, lenders, and insurance carriers.

The Cost of Not Planning

Without proper liquidity planning, heirs may be forced to:

-

Sell Real Estate

-

Sell Businesses

-

Liquidate Investment Portfolios

-

Trigger Capital Gains Taxes

-

Disrupt Long Term Investment Strategies

Strategic planning helps families prepare for these events before they occur.

Before vs After Estate Liquidity Planning

This comparison illustrates how estate liquidity planning strategies may help families avoid forced asset sales by providing liquidity through structured life insurance planning.

Why Families Work With Strategic Premium Finance

-

Coordination with CPAs and Estate Attorneys

-

Conservative Underwriting Assumptions

-

Structured Bank Financing Strategies

-

Coordination with Lenders and Carriers

-

Conservative Premium Financing Structures

-

Long Term Monitoring and Exit Planning

Premium Financing Exit Strategy Diagram

This diagram explains potential exit strategies for premium financing structures including loan repayment through policy cash value, policy maturity, or death benefit proceeds.

Who This Strategy Is Typically Designed For

Premium financing structures are generally considered for individuals who:

-

Have a Net Worth of $5M+

-

Have Strong Income or Balance Sheet Strength

-

Maintain Long Term Investment Horizons

-

Work with Professional Advisors on Estate Planning

-

Own Significant Real Estate Holdings

-

Operate Privately Held Businesses

-

Maintain Concentrated Investment Portfolios

-

Expect Future Estate Tax Exposure

-

Hold Wealth in Illiquid Assets such as Businesses or Real Estate

Each situation requires individualized analysis before determining whether the strategy is appropriate.

Evaluating Estate Liquidity Planning Strategies

Families whose wealth is concentrated in businesses, real estate, or long term investments may benefit from evaluating estate liquidity planning options well in advance of potential tax obligations.

Strategic Premium Finance helps clients and their advisory teams explore whether structured premium financing strategies may fit within their broader estate planning framework.

Common Uses of Premium Financing

Premium financing is often used to:

create estate liquidity

fund life insurance inside trusts

reduce pressure to sell assets

support generational wealth transfer

complement business and investment planning

Request a Confidential Strategy Session

If you’re exploring whether premium financing could fit into your broader planning strategy, the first step is a brief confidential consultation.

No obligation. Just clarity.

Book Your Free Private Strategy Call

Confidential. No obligation.

- (305) 903-0363

- Marc@strategicpremiumfinance.com