Estate Liquidity Planning | Preserve Wealth Without Selling Assets

Estate liquidity planning for high net worth individuals with assets concentrated in businesses, real estate, and long term investments.

Evaluated in coordination with CPAs, estate attorneys, and financial advisors.

Built for business owners, real estate investors, and high net worth families with estate liquidity exposure. Coordinated with CPAs, estate attorneys, wealth advisors, carriers, and lending institutions.

The Estate Liquidity Problem

Estate taxes and other obligations are based on total asset value not liquidity. When wealth is concentrated in businesses, real estate, or long term investments, a gap can exist between what is owed and what is available.

Why This Matters

A strong balance sheet does not guarantee liquidity. Without planning, obligations may require:

- Selling Business Interests

- Liquidating Real Estate

- Disrupting Long Term Investments

A Structured Approach to Estate Liquidity

Strategic Premium Finance evaluates whether premium financing can be used as part of a broader estate liquidity strategy.

In certain situations, this structure may allow life insurance premiums to be funded with external capital rather than requiring asset liquidation.

These strategies are not universally applicable and are evaluated within the context of a client’s broader financial structure, liquidity profile, and long term objectives.

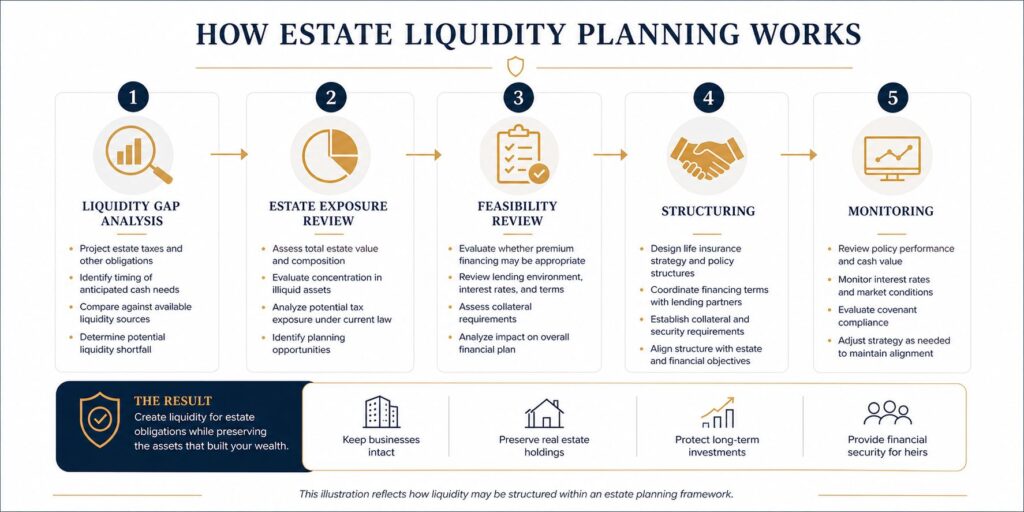

How Estate Liquidity Planning Works

This illustration reflects how liquidity may be structured within an estate planning framework.

Who This Strategy Is Designed For

- $5M+ Net Worth

- $300K+ Income

- Asset Concentration

- Long Term Horizon

This is not designed for individuals seeking short term strategies or basic insurance solutions.

Important Considerations

Premium financing involves financial leverage and requires careful evaluation of interest rates, collateral requirements, and long term policy performance.

These structures are typically monitored and adjusted over time within a broader planning framework.

Built for Advisor Collaboration

Strategic Premium Finance works alongside CPAs, estate attorneys, lenders, and financial advisors to evaluate and structure liquidity strategies within a broader planning framework.

Illustrative Planning Scenarios

Different clients face different forms of estate liquidity exposure. A business owner with concentrated company equity faces a different planning challenge than a real estate investor, an ultra high net worth family, or a household with concentrated market positions.

Explore illustrative planning scenarios that show how estate liquidity strategies may be evaluated across a range of wealth structures.

Not Sure If This Applies to Your Situation?

Every estate structure is different. The right planning approach depends on your asset mix, liquidity position, estate exposure, planning horizon, and advisor coordination.

A confidential review can help determine whether structured liquidity planning deserves further evaluation.

Frequently Asked Questions

Estate liquidity planning ensures there is cash available to pay estate taxes and expenses so assets like real estate or businesses don’t have to be sold under pressure.

Estate taxes are typically due within 9 months after death. They are paid in cash, which often forces families to sell assets quickly if proper planning isn’t in place.

Premium financing is a strategy where a third party lender finances life insurance premiums, allowing capital to remain invested while still providing future liquidity.

Premium financing is a structured strategy with risks, but when properly designed and monitored, it can be an effective way to create liquidity without using large amounts of personal capital upfront.

This is designed for high net worth individuals and families who have significant assets but want to avoid forced sales and protect long term wealth.

Most premium financing strategies are designed for individuals with strong income, substantial net worth, and long term planning horizons.

Yes. Interest rates are a key factor in premium financing. Conservative design, stress testing, and ongoing monitoring help manage this risk

No. These strategies are evaluated selectively based on financial profile, asset structure, and long term objectives.

Often yes, especially for estate and legacy planning.

These structures are most often used by business owners, real estate investors, and high net worth families whose wealth is concentrated in illiquid assets.

No. This approach is designed to work alongside your CPA, estate attorney, and financial advisor not replace them.

Estate Liquidity Planning May Involve Tax, Legal, And Financial Considerations

- IRS estate and gift tax information

- Federal estate tax resources

- Trust and estate planning education

- Financial industry investor education

Start With a Structured Review

A confidential evaluation designed to determine whether estate liquidity strategies may align with your current balance sheet and long term objectives.

These strategies are evaluated selectively and are not appropriate for all financial profiles.

Book Your Free Private Strategy Call

Confidential. No obligation.

- (305) 903-0363

- Marc@strategicpremiumfinance.com

Begin Your Estate Liquidity Planning Process

Understanding the estate liquidity planning process allows you to make informed decisions with confidence and control.

Estate liquidity planning is not about making immediate decisions.

It is about understanding your position clearly and evaluating the right structure if one is needed.

The first step is simply a conversation.

Book Your Free Private Strategy Call

Confidential. No obligation.

- (305) 903-0363

- Marc@strategicpremiumfinance.com